35+ Essential Auto Loan Statistics (2023 Update)

Purchasing a car is often treated as a financial burden since both used and new cars can be pretty expensive, depending on their brand, make, specs, and model year. At this time, numerous people throughout the world choose to purchase new and used cars via auto loans — a personal loan where the proceeds are used to purchase a vehicle. Similarly, understanding everything there is to know about auto loans is bound to be quite difficult, given the plethora of information on the subject, alongside discrepancies in terms of the average car loan, types of auto loans, payment plans, average monthly rates, financing periods, and more.

As such, finding the right car, and the proper way to finance it, generally entails that purchasers do their due diligence thorough research to ensure they get the best auto loan possible. With this in mind, this article is meant to highlight some of the industry’s most relevant statistics, to help paint a clearer picture of how much Americans owe to car loans, the average loan amount in the US, the number of annual car loans, the average loan length, the demographics, the required credit scores, and much more.

Must-Know Auto Loan Statistics (Editor’s Picks)

- US citizens are currently dealing with roughly $1.18 trillion in car loans.

- In 2019, the average US loan amount for a new vehicle was estimated at $32,187, and $20,137 for used cars.

- The total number of newly-signed car loans in the United States was record-high in 2016 when over 27.54 million loans were taken.

- Despite the fact that auto loans account for only 9.28% of America’s credit, 85% of newly-purchased non-commercial vehicles are financed in the US.

- The average term for auto loans is 69 months, in the case of new vehicles, and 65 months for second-hand cars.

Auto Loan Statistics in the US

1. The monthly cost for new vehicles in the US is $550.

On average, the monthly cost in the US is $550 for new vehicles, $452 for leased vehicles, and $393 for used vehicles.

2. The auto loan delinquency rates in 2020 dropped compared to last year.

Both 30-day and 60-day auto loan delinquency rates in 2020 dropped in comparison to 2019.

The 30-day delinquencies experienced a drastic decrease from 1.98% in the first quarter of 2019 to 1.93% in the first quarter of 2020. Research also showed that 60-day delinquencies dropped from 0.68% in 2019 to 0.67% in 2020.

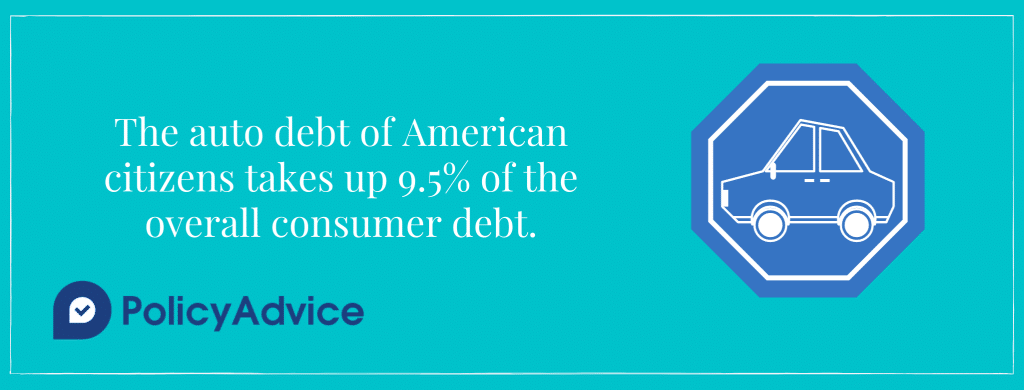

3. The amount of auto loan debt accumulated by Americans is alarmingly high, crossing the $1.2 trillion mark in January 2020.

The auto debt of American citizens takes up 9.5% of the overall consumer debt.

Due to the high auto loan rates, reports have shown that Americans owe trillions in auto loan debt. The overall cost of the auto loan debt of Americans has increased 75% since the end of 2009.

4. Americans take out more than $50 billion in auto loans.

Statistics show that around $56 billion across more than 2 million new car loans are taken out by Americans every month.

5. Americans take out a $32,480 loan for new vehicles.

The statistics on US auto loan rates show that, on average, Americans borrow $20,446 for used vehicles and more than 31,000 for new ones.

6. The loan term for new cars is 69 months.

On average, the loan term is 37 months for leased vehicles, 35 months for used cars, and 69 months for new cars. Reports have shown that 4.5% of outstanding auto debt is about 90 days late, and 7% is overdue for 30 days.

7. In 2019, the auto loan APR was more than 8%.

The auto loan annual percentage rate (APR) in 2019 was 8.06%. However, this percentage ranged from 5.66% on average for borrowers with strong credit and 21.54% for borrowers with bad credit.

8 Americans aged 45 and younger can take out an auto loan for about $38 million.

If you are 45 years old or younger, you can take out an auto debt for $38.1 million. In comparison, Americans older than 45 can take out $13.3 million.

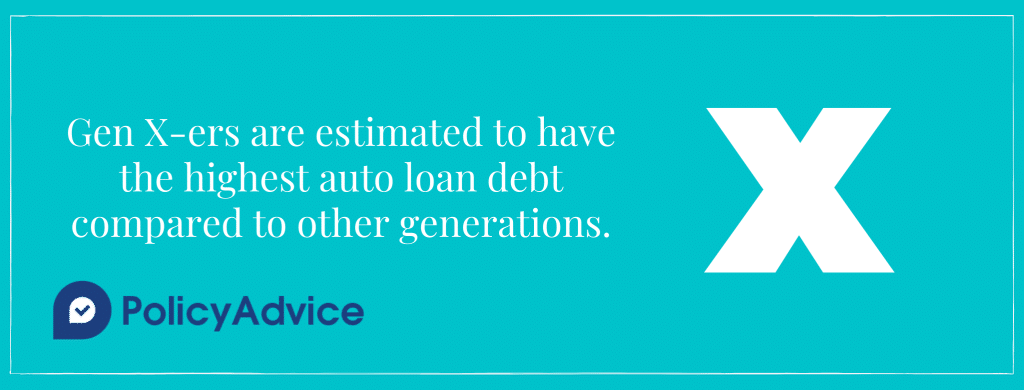

9. Gen Xers are estimated to have the highest auto loan debt compared to other generations.

According to statistics, the individuals in Generation X have the highest possibility of having a car loan and owe the highest balances than other generations, with an average of $19,313.

10. The cost of a light-duty new car is on average $38,948.

This cost is a 1.7% increase from the price at the end of 2018. The cost for used cars averages almost half of the price of the new cars – $20,683.

11. The interest rate on a five-year car loan was the highest at 4.96% by the end of 2018.

The interest rate on a five-year car loan gradually increased in the past years, reaching the highest in 2018 with 4.96%. It was over 4% by the end of November 2020. The financing for new cars was around $32,797 on average by the last quarter of 2019.

12. In the first few months of 2020, the auto loan debt reached $1.17 trillion in the US.

Reports show that the outstanding auto loan debt in the first quarter of 2020 amounted to $1.17 trillion.

13. The 2009 financial crisis led to a drop of the interest rate by 40%.

According to auto loan origination statistics, the interest rate on an auto loan of 48 months dropped more than 40% in the last decade.

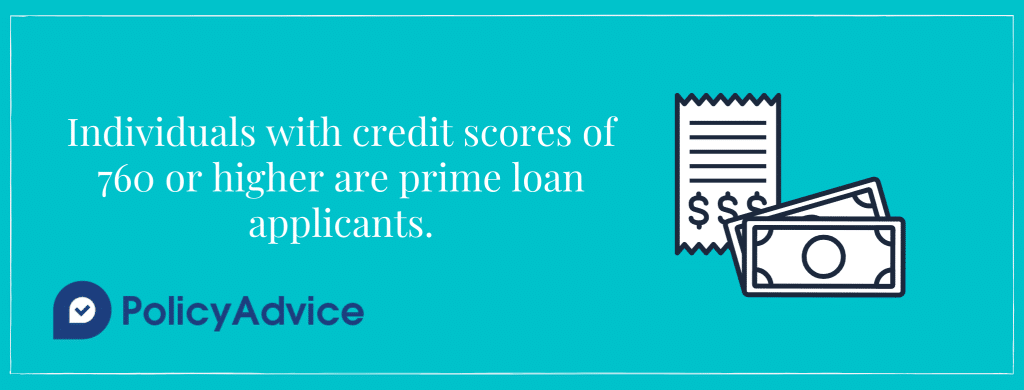

14. Individuals with credit scores of 760 or higher are prime loan applicants.

These consumers get approved for loans with interest rates that are as low as 3%. The people with low credit scores end up paying an interest rate as high as 20% as they are a riskier investment.

15. The auto loans during the pandemic experienced a dramatic drop.

Due to COVID-19, the rates of auto loans have decreased. This drop is expected to increase auto sales just as it happened during the 2008 recession.

16. In 2019, estimates show that US citizens are dealing with roughly $1.18 trillion in car loans

Over the last couple of years, we notice an increasing trend in the total amount of car-related debt at the US level. The large number alongside the increasing trend is quite understandable given the fact that there are approximately 276 million registered vehicles operating on US roads, according to auto loan statistics. This seems to be a 6.5% increase when compared to 2018’s first quarter.

Source: Experian

17. An Experian study indicates how the overall outstanding auto-related loan debt has increased over the years

As such, $1.01 trillion was owed in 2016, followed by $1.10 trillion in 2017, $1.11 trillion in 2018, and $1.18 trillion in 2019. This trend is likely to continue as long as the economy remains within similar parameters. Therefore, there is considerable joy in the case of institutions offering car loans, given the vast amount of auto debt.

Source: Experian

18. In 2019, the average US loan amount for a new vehicle was estimated at $32,187

With this in mind, we can conclude that American car lending sums are higher when compared to other regions of the world, where people generally tend to finance cheaper vehicles. Considering that the average loan term is currently 69 months, we get an average monthly payment of $554 for new cars; the average car payment in America for 2018 was lower.

Source: Experian

19. In 2019, the average US loan amount for a used vehicle was estimated at $20,137

This statistic helps demonstrate that loans for used vehicles are generally much lower when compared to the amounts being lent out for new cars. In this case, the average monthly payment is only $391, whereas the general loan term duration is 64.7 months, as indicated by stats concerning the average US car payment.

Source: Experian

20. The average loan for new vehicles increased by $733 when compared to 2018, hitting a new record; the average loan for used vehicles also reached a new high, following a $601 increase when compared to 2018

Based on this statistic, it seems that Americans are now paying at least $500 more on loans for new and used cars. While loan rates, terms, and monthly payments have stayed roughly the same, loan amounts are steadily increasing, according to statistics on the typical car loan.

| Average Loan Data (for Q1 2019) | New Car | Used Car |

| Loan Term | 68.9 months | 64.7 months |

| Loan Rate | 6.16% | 10.06% |

| Loan Amount | $32,187 | $20,137 |

| Monthly Payment | $554 | $391 |

Source: Experian

Total Number of Car Loans in the US by Year

21. The latest statistical data shows that roughly 27 million new car loans were signed during 2018

As such, we can conclude that most Americans purchase new cars through financing, rather than upfront. As we will see later on, the number of new car loans is increasing; therefore it is likely that the 30 million thresholds will be reached sometime during the next decade — possibly as electric cars gain in popularity, as shown by auto loan statistics.

Source: Lending Tree

22. In 2017, Americans signed roughly 183,000 fewer loans when compared to 2018

This statistic once again proves the increasing trend in terms of vehicle loans. However, it isn’t only the number of loans that are increasing, but also the actual amount connected with the loan, as outlined earlier. The incidence of lower auto lending rates varies based on the current car debt market conditions.

Source: Lending Tree

23. The total number of newly-signed car loans in the United States was record-high in 2016 when over 27.54 million loans were taken

So while the numbers briefly dropped from one year to the next, the US auto loan market is still standing strong. Numerous analysts have tried to find the reasons behind these changes. Truth be told, it is a series of factors, including (but not limited to) the release of new cars by manufacturers, a more powerful economy, better deals from auto traders, alongside varying lending conditions for the average car payment.

Source: Lending Tree

24. At this point, it is believed that auto-related loans account for roughly 10% of overall US-based outstanding consumer debt

This makes perfect sense considering the millions of loans Americans have taken up to purchase new or used vehicles. Financing options have therefore become more attractive, but it is still imperative for future car loan contractors to ensure they have the means to cover the average monthly car payment since numerous outstanding car-related loans are already extremely late.

Source: Lending Tree

25. In 2017, there were 108.66 million car loan accounts opened by Americans

According to statistics provided by NewYorkFed, these numbers are also steadily growing. Consequently, there were 103.69 million accounts in 2016, 97.14 million in 2015, 81 million in 2012, 80.9 million in 2010, and 74 million in 2013.

Source: NewYorkFed

Average New Car Payment vs Used Car Payment

26. In 2017, the average amount taken for loans for purchasing used cars at franchises was $21,375

We have a monthly payment of approximately $398 for used cars during the year 2017. Do keep in mind, though, that this statistic is exclusive to franchises, which are dealerships that have been authorized for resale by the manufacturers; just one of many well-known car loan facts.

Source: Finder

27. In the case of independent dealers, the average loan amount for second-hand car purchases was of $17,002

With this in mind, we can see that buying a car at a dealership franchise is bound to be a more expensive endeavor. The general reason for this price spike is the fact that franchise dealerships tend to offer vehicles that have been thoroughly inspected from a technical point of view. Similarly, these vehicles also come with more advantageous deals for maintenance and auto insurance, as reported by car loan statistics.

Source: Finder

28. Used cars purchased at an independent dealership usually come with an average monthly payment of $348

This number is based on the higher interest rate associated with independent dealerships, yet tends to depend on how much you are willing to put aside as a down payment, alongside the actual duration of the loan, as indicated by trends concerning the average car payment in 2019, but also in previous years.

Source: Finder

29. New cars come with an average interest rate of roughly 5.11% per year in the US

Of course, the actual interest rate that users will be paid when taking a car loan depends on their credit score, down payment amount, the price of the car, and the general conditions imposed by the lender. It is worth pointing out that budget cars usually have lower interest rates.

Source: Finder

30. The average interest rate for franchise used cars is estimated at 7.68%, and 11.48% for used cars purchased at an independent dealership

With this in mind, purchasing a used car at a franchise is generally bound to be cheaper. The downside here is that when searching for a vehicle, you will have fewer cars to choose from since authorized franchises generally carry the cars of only one manufacturer.

Source: Finder

Auto Loan Debt and Other Major Debts

31. At this point, an average US citizen has $38,000 in debt (without mortgages), whereas the total household debt was estimated at $13.21 trillion following a study in 2018

It is also important to mention that the biggest sources of debt in the US are credit cards, mortgages, and student loans. Fewer Americans hold as much automobile loan debt as they hold personal or mortgage debt. This is why many financial experts recommend sticking to a budget car until settling a significant percentage of outstanding debt.

Source: Debt.org

32. A Finder study found that auto loans accounted for roughly 9.28% of America’s debt in 2017

In other words, over 90% of American debt comes from other sources, such as credit cards, personal loans, mortgages, student loans, and more. These figures vary from year to year, yet mortgage debt has consistently remained the highest source of debt for the US economy, unlike your average car loan.

Source: Finder

33. The percentage of debt balance held by auto loans has varied considerably through time. Here are some relevant numbers:

– 2017: 9.03%;

– 2015: 7.84%;

– 2012: 6.18%;

– 2007: 7.41%;

– 2003: 9.27%.

Source: Finder

34. For the sake of comparison, mortgages account for 67.63% of US debt, followed by 10.5% for personal debt, 9.28% for auto loans, 6.17% for credit cards, and 3.48% for home equity credit lines

This statistic also helps illustrate the main priorities in the lives of Americans, alongside their lending habits. However, mortgages are more common as people age, and their monthly gross income increases.

Source: Finder

35. Despite the fact that auto loans account for only 9.28% of America’s credit, 85% of newly-purchased non-commercial vehicles are financed in the US

Hundreds of millions of vehicles have been purchased thus far by customers leveraging various financial options (loaning and leasing overpaying lump sums with cash). Similarly, the same study has concluded that 55.5% of second-hand vehicles are also financed in the US.

Percentage of Financed Vehicles 2018-2019

New Cars 85.3% 85.4%

Used Cars 54.0% 55.5%

Source: Experian

Average Car Loan Length

36. At this point, it seems that the average term for auto loans is 69 months in the case of new vehicles

In other parts of the world, car buyers tend to choose shorter financing periods, to get rid of all the accumulated debt as soon as possible. However, it seems that US-based car loan providers, such as Bank of America auto loans, offer sweeter deals that include mostly long-term financing options.

Source: Lending Tree

37. In the case of used car loans, estimates show that the average term for this debt is 65 months

As you can see, there is no significant difference when considering whether to get a new or used car loan. Based on this, for both types of cars, the typical auto loan term is approximately 5 to 6 years.

Source: Lending Tree

38. It seems that people with middle-tier credit scores have the tendency of signing loan terms of approximately 73 months

This makes sense, since getting a bad credit score is usually a result of not paying past credits on time, or having a lower income. Therefore, given the lower-income, it only makes sense that people in this category take longer loans. It is, important to mention that longer loans are often associated with a higher interest in the end. Hence, when answering the question “how much is the average car payment,” it might be higher for long-term car loans.

Source: Lending Tree

39. Borrowers who have good credit scores have the tendency of taking short-term loans, of approximately 63 months

This statistic presents the fact that top-credit borrowers usually have no trouble in taking short-term loans and paying them back on time, given their history of on-time payment and higher income. In cases like this, the average car loan payment may be lower.

Source: Lending Tree

40. According to the Federal Reserve Bank of New York, it seems that roughly 7 million Americans are at least 90 days late in paying their vehicle loans

Consequently, these individuals are classed as loan delinquents and face the risk of worsening credit scores, as well as having to pay additional fees for being late, leading to increased average new car interest rates. Reports indicate that between 2012 and 2019, the rate of delinquent loans increased from 1.5% for auto loans, up to 2.4%. The same report also indicates that it is young buyers who are mostly struggling with their monthly car payments. This makes sense, given the fact that numerous younger adults also have to deal with student loans, which usually take a few years to get paid back in full.

Source: BankRate

Car Loan vs Lease Statistics

41. An Experian report indicates that roughly 29.1% of passenger cars were purchased through a leasing agreement in the first quarter of 2019

While both car loans and leasing are highly-popular on the US market, vehicle loans are slightly more popular. The main difference between the two is that in the case of a car loan, you become the owner of the vehicle once the purchase is made — thus, you enter an automobile debt contract. As a result, you must pay off your monthly rates. On the other hand, when leasing, you get the option to purchase the car at the end of the leasing period if you can afford it. Failure to afford to purchase the car has fewer consequences in this case since you will only be charged a monthly fee for renting the car. In this sense, a car lease can be more advantageous.

Source: Experian

42. The average fee for a US vehicle purchased by leasing is around $457 per month in 2019

This price represents an increase when compared to last year when the monthly leasing rate was roughly 5% lower. Therefore, similarly to car loan payments, leasing monthly rates also tend to vary from year to year. As such, this isn’t a very important factor to consider when choosing whether to lease or buy a car.

Source: Experian

43. Monthly leasing rates are approximately $97 lower when compared to monthly car loan payments

This statistic helps us conclude that indeed, purchasing a car via a loan is bound to be more expensive, yet it ensures ownership from the start, unlike leasing. At this point, there are numerous factors to consider when trying to determine the average used car payment per month in America. In the case of leasing, terms are also shorter, since approximates indicate that the average leasing period is 36 months.

Source: Experian

44. 27 million auto loans were taken in 2018, whereas leasing accounted for 29.1% of all new vehicles sold in the United States

Making the right decision between leasing and lending depends mostly on the types of financing provided by your auto dealership of choice. Many people tend to choose auto lease given the fact that in this case, the depreciation cost is absorbed by the leaser, not the customer as one would think.

Source: Statista

45. An Experian study carried out during the first quarter of 2019, concluded that the Honda Civic was the most leased passenger car in the United States

Numerous other models were purchased in leasing as well, yet the Honda Civic holds a 3.7% market share. The average length of a car loan or lease for Honda Civic ranges between 4.5–6 years. Some of the other popular models of cars that are purchased with leasing include the Chevrolet Equinox at 3.3% market share, Honda CR-V at 3.1% market share, Honda Accord at 2.9% market share, Jeep Cherokee at 2% market share, and the Ford F-150 at 1.7% of the leased cars market share.

Source: Experian

Car Loan Debt, Demographics, and Credit Score

46. A recent study has determined that in the US, baby-boomers are the demographic accounting for most new car purchases

In fact, in the first quarter of 2019, baby-boomers reportedly registered 32.2% of new vehicles in the US. Millennials represent the second group of new car buyers, given their 28.6% market share, followed by Gen X with a 27.1% market share. Factors like the typical auto loan term haven’t been taken into consideration when this ranking was created.

Source: Experian

47. The demographics accounting for the lowest number of new vehicle registrations are the silent generation, holding 8.3% of the market share, and Gen Z purchasers, holding 2.8%

This statistic shows that there is huge income inequality between generations. Indeed, better prospects and higher yearly income both come with age and increased experience. However, younger adults shouldn’t have to face strong financial hardship when purchasing a new vehicle, nor should they always stick to budget cars.

Source: Experian

48. At this point, most vehicle loan companies look for buyers with a credit score situated around the 707 threshold

People with higher credit scores generally get access to better financing options, alongside higher rates for loan approval. With this in mind, if you hold a credit score above the 707 thresholds, it is important to remember that the average vehicle loan interest rate may also be lower.

Source: Finder

49. In 2017, roughly 30.97% of auto loans were given to people with a credit score above 760

On the other hand, individuals with lower scores also managed to secure a significant portion of vehicle loans. Here are a few relevant numbers reflecting the situation in 2017:

Credit Score Percentage of Loans

720–759 14.83%

660–719 22.07%

620–659 12.15%

<620 19.98%

Based on this, unless your credit score is very low, getting a car loan shouldn’t be too difficult. Yes, the average interest rate for the car loan will be higher, but being approved is certainly possible. Of course, if you wish to further reduce your interest rates while accessing better financing conditions, you might first want to research methods of increasing your credit score. At this point, there are numerous online resources offering valuable information on how to budget better, but also on how credit scores work. These resources are therefore a gold mine if you want to access an average vehicle loan interest rate.

Source: Finder

50. A MarketWatch study has analyzed the current size of automobile loan debt across the US and determined which states face the highest amounts of debt

Texas ranks first, with an automobile loan debt balance per capita of $6,700, followed by California with $5,700, Georgia with $5,400, and New Hampshire with $5,300. On the other side of the spectrum, we have US states where people tend to buy budget autos. States in the northeastern parts of the US tend to have the lowest amount of vehicle debt balance per capita. For instance, the District of Columbia has an average loan balance of just $3,000, while other states with low debt include Michigan, New York, and Kentucky, where the debt balance ranges between $3,700 and $4,000. With these aspects in mind, we can conclude that the average American car payment tends to vary from state to state.

Source: MarketWatch

Bottom Line

In the end, most of the new (85%) and used cars (55%) that are sold in the United States are purchased using a financing option (leasing or passenger vehicle loans). Thus, the auto financing market is bound to grow within the next couple of years, as numerous Americans prefer lending or leasing, rather than paying for the car upfront. Despite this feature, the average car payment in 2018 and 2019 has increased, meaning that more money is invested in new vehicles at the US level.

Last but not least, we hope that our statistics have helped paint a clearer picture of the US vehicle market at this point. Similarly, we also hope that we have outlined some of the industry’s problems, such as the fact that young adults can hardly afford to purchase new cars, while interest rates still depend on credit scores.

From a long-term perspective, we can predict that the loan prices will fluctuate considerably, just like the economic input and output of the US.

FAQs

What is the average monthly car payment in the US?

The average payment in 2019 was $32,000 for a new car and $20,000 for a used vehicle.

What is a good rate for a car loan?

At this point in time, the average loan rate for new vehicles is estimated at 6.16%. In the case of used vehicles, the loan rate is approximated at 10.06%.

Is a 72-month car loan bad?

To answer this question we must first answer: what is the average length of a car loan. Most new and used vehicles are purchased in less than 70 months, meaning that most people sign contracts with loan terms that are shorter than 72 months. Generally, the longer the term, the more you will pay for the car in the end; even if you go for a lower interest rate, it will all add up by the time you finish with the payments.

How long is the average car loan in the US?

Experian reports estimate that the average loan term is estimated at 68.9 months for new vehicles and 64.7 months for second-hand cars.

Why financing a car is a bad idea?

Credit overall is a bad idea since it means you cannot afford the product in question. Economic analysts indicate that taking debt is risky; purchases should mostly be made upfront.

However, in the real world, this is almost impossible. Generally, it is best to finance cars only if you are fully certain that you can afford the monthly rate, while also accounting for GAP insurance and other costs.

What is the average car payment in 2020?

The average car payment in the US in the second quarter of 2020 was $397 per month for used cars and $568 per month for new cars.

Why should you never finance a car?

The major reason you should never finance a car is that it is a bad investment, and your warranty is most likely to run out even before your loan payment is over.

Is $400 a month too much for a car?

On average, Americans pay $568 every month for a new car and $400 every month for a used car. These statistics show that $400 every month is not too much for a car, but of course, it depends on the model, make, and condition of the car.

List of Sources: